_(9353348720).jpg){kind=link}

If you threw a rock in a room full of African startup founders today, you would likely hit one offering to give users loans “in just 10 minutes!” via their mobile phones. This should not surprise you; in the past 24 months, we have witnessed a windfall for fintech startups on the continent, with investors deploying more capital into the sector than anywhere else.

The problem they aim to solve is well-documented. Many consumers in emerging markets operate entirely outside the formal financial ecosystem. They are financially ‘excluded’, and in response, startups hope to harness mobile technology to ‘include’ them in the formal economy. There is little infrastructure to ‘disrupt’, so these startups must build it. Take lending. Today’s formal financial systems are designed around predictability; a certain amount of money called “salary” shows up on schedule every month, and stability; this salary comes from the same source [1]. The bank’s risk assessment methods only support giving loans against this consistency. But these conditions are increasingly not true for the average consumer in developing markets. Income is irregular and unpredictable, and most transactions happen offline via cash, other signals must be used to determine creditworthiness.

Fintech startups are betting big that they can accurately figure out who can and will repay unsecured loans, offer those loans to them directly, circumvent the traditional institutions who have failed so far, and build new financial ecosystems around themselves.

But one company, Mines, has just raised a $13 million Series A round to do the exact opposite.

All Men Are Not Equal

The dominant narrative in startups today closely tracks the story of the demise of knights. In the Tudor period (1485 - 1603), the English Renaissance brought new philosophy, new art, and new literature. Henry VII took the throne like you would expect a 15th century monarch to: noble knights on horseback engaging in chivalric combat. Being a warrior in those days required years of intense training and mastery of handheld weapons like swords, and axes, and war hammers.

Battle of Bosworth by Philip James de Loutherbourg (1804); This is where Henry VII won the Wars of the Roses.

But the Renaissance also brought new technology. By the end of Elizabeth I’s reign - the end of the Tudor period - battles were won by siege warfare [2] and projectile weapons like crossbows, cannons, and muskets. Times had changed, but medieval knights could not keep up. The result was that all men were made ‘equal’. Knights and castles that were once impenetrable were now vulnerable to armies of barely-trained peasants with bows and guns. The knights had become [3] ‘priests of a dead religion’, and became obsolete as the grounds of warfare shifted beneath their feet. The things that once made them powerful were now their greatest handicaps (e.g., reinforcing their breastplates to withstand bolts and arrows, would have made them too heavy to carry). They were - to misuse the term as we often do - disrupted.

In the same way, accepted wisdom says [4] the battle between startups and incumbents comes down to whether the startups get distribution before the incumbents gets innovation. “The large corporations are not nimble enough!”, the narrative goes. “Innovate or die!” “Startups will disrupt you, and you will be disrupted!” Mobile, specifically enabled by internet connectivity, is changing the nature of markets, and enabling young companies in Africa compete ‘unfairly’ with old, large institutions. But instead of competing with legacy players, Mines is trying to empower them.

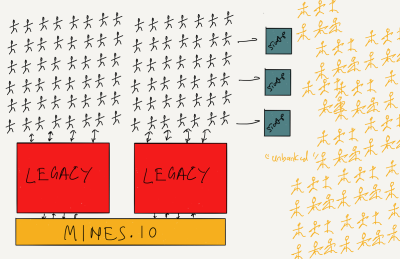

This is the conventional fintech/digital credit startup:

Illustrated by Osarumen Osamuyi for The Subtext

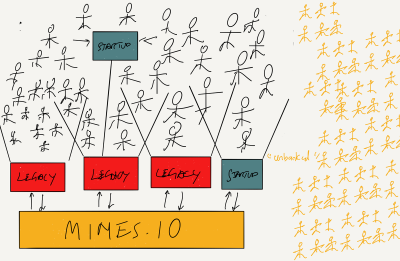

This is Mines:

Illustrated by Osarumen Osamuyi for The Subtext

It is taking all the component parts of a credit product (risk assessment, disbursement, loan management, collections, etc.), putting them in a bundle, and selling that bundle to large firms - banks, mobile operators, big retailers, and payment processors - in theory, instantly giving them the ability to offer credit to their users.

Mines started in 2014 as an AI research project by Stanford Professor, Kunle Olukotun, who partnered with Ekechi Nwokah, then a Principal Security Engineer at Amazon AWS, to apply the technology to risk assessment for financial services. Since then, they have integrated with 9Mobile (FKA Etisalat), a Nigerian telco operator to launch Kwikcash, disbursing 4.5 billion naira ($12.5m), with an average ticket size of 12,000 naira ($33) in the past 18 months, according to MD, Nigeria and VP Commercial, Adia Sowho, ex Director of Digital Business at 9Mobile. She reckons they are the largest credit platform in Nigeria today. (The company has also penned partnerships with Airtel, and payment processor, Interswitch.)

MINES Executives. L-R: VP Commercial, Adia Sowho; CEO, Ekechi Nwokah; Chief Scientist, Kunle Olukotun

Competition by Ecosystem

Remember the above quote: “the battle [...] comes down to whether the startups get distribution before the incumbents gets innovation”. Mines - in theory, at least - is handing innovation on a platter to banks, telcos, large retailers, and payment processors. The knights are getting guns, too!

By offering them credit-in-a-box, Mines is sacrificing data ownership and a direct relationship with the consumer for faster - better - distribution. But why is this the right approach? Their pitch to their clients is that they [Mines] have built better technology than they [clients] can build, and that they [Mines] have a better product than other consumer players can deliver. If that is true, why not take this ‘better’ product directly to the consumers and beat everyone else? Isn’t this the more valuable position in the value chain?

I posed this question to Adia (she was kind enough to join me for a drink a few days ago), and she argued that partnerships are the most effective path to scale in these emerging markets. I see the logic here, and mostly agree. Big corporates own distribution today and thus, have most of the leverage. Consumer markets are shallow, and mobile penetration has not yet delivered its great promise of integrating fragmented markets. (We will talk more about this soon.)

But in taking this approach, Mines is also doing two things:

- Commoditizing credit scoring and sucking out air for smaller startups, forcing them to look elsewhere for growth. For example, almost all digital credit/fintech apps in Nigeria offer bill payments and airtime purchases as a feature, ensuring that nobody will switch apps to access that feature. The same might happen with credit.

- Creating the opportunity for Mines to create an ecosystem of ecosystems; powering even other fintech startups. This would provide the opportunity for, say, Piggybank or a service to quickly launch a loans product like I predicted in Issue #1 (I admit, confirmation bias might be getting to me here...).

If the above is true, then we will arrive here:

Illustrated by Osarumen Osamuyi for The Subtext

Mines' Many Markets

This is the big opportunity. Mines’ many markets are not the countries it plans to expand into (though, the company’s leadership have taken pains to communicate that they serve ‘emerging markets’, not ‘Nigeria’ or ‘Africa’), but all the different businesses, each with their own pool of customers, who will operate their own financial ecosystems with Mines at the base. Some of these customers will use products from more than one Mines client, helping Mines get better at identifying good borrowers, and forming credit-scoring infrastructure.

But therein lies my main reservation; by relying on its partners for its data and its growth, Mines both extends its reach and limits its grasp. Today, like most other consumer credit platforms, the company’s flagship product, Kwikcash requires users to have BVN (Bank Verification Number), and thus, bank accounts. There are 30 million of them in Nigeria (population: 190 million). Hard cap. The next ceiling is the number of mobile subscribers in the country, which most people peg around 60m today (subscriptions are 90m). Adia acknowledged these limitations, when I asked about them, but ultimately trusts Ekechi and Tunde to work out what’s next (“the company was founded by computer scientists, and today, we are already thinking about what new signals to incorporate”). We will see if they do, but there is cause for skepticism today.

Mines certainly could create value for itself and its partners within their ecosystems - and, to be clear, this seems a big enough opportunity to make it worth the while - but it is placing a bet on the old and established. Tethering itself to legacy players; going where they go, growing where they grow, is a smart path to ‘scale’ in these markets, admittedly. But whether the company will achieve its own stated goal to provide access to credit for 3 billion people depends on who ultimately wins: the knights, or the peasants.

--

That’s all for today.

Thank you for reading! Please tell someone about The Subtext if you like it, and tweet at me to give feedback.

With love in my heart and Famous Amos cookies in my belly,

Osarumen.

REFERENCES

- Bhan, N. (2016) Unlearn The Past To Create The Future. http://nitibhan.com/2016/11/06/unlearn-the-past-to-create-the-future/

- Barber, Richard W. The Knight and Chivalry. Ipswich: Boydell, 1974.

- Schwope, D. (2004) Death of the Knight: Changes in Military Weaponry during the Tudor Period. Henderson State University https://www.hsu.edu/academicforum/2003-2004/2003-4AFTheDeathof%20the%20Knight.pdf

- Rampell, A. (2015) Distribution vs. Innovation. Andreessen Horowitz https://a16z.com/2015/11/05/distribution-v-innovation/